Nigeria recorded a sharp reduction in the gender gap in mobile money account ownership in 2025, even as disparities persist globally between awareness and actual usage, according to a new report by the GSMA.

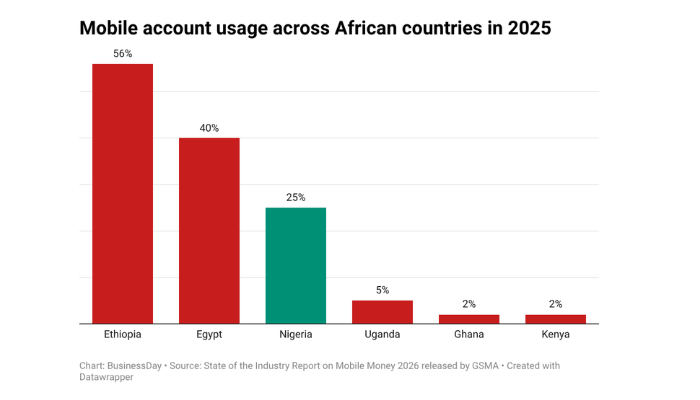

The State of the Industry Report on Mobile Money 2026, Nigeria, however, stands out for its progress. The gender gap in mobile money account ownership declined significantly to 25 percent in 2025, down from 41 percent in 2024 and 46 percent in 2023.

“The improvement was driven by a 21 percentage-point increase in women’s account ownership, with nearly half of adult women now owning a mobile money account,” the report disclosed.

Read also:Mobile money hits $2trn global milestone in 2025 after doubling in four years

Despite growing awareness of mobile money services worldwide, ownership remains uneven, particularly among women. The report noted that mobile money awareness does not necessarily translate to account ownership, highlighting a persistent drop-off along the user journey.

In several countries, this gap remains pronounced. Pakistan records a gender gap of 63 percent, with only 13 percent of women owning an account compared to 35 percent of men. Ethiopia, where adoption rates are 13% for women and 29% for men, comes in second with a 56% difference. Egypt also shows a sharp drop from awareness to ownership, while Sri Lanka records the lowest levels of account ownership among newly surveyed countries.

The broader trend suggests that the gender gap in mobile money account ownership has widened in the past five years, although recent data indicates early signs of improvement in some markets.

Also, countries such as Nigeria and Egypt are beginning to reverse this trajectory. In Egypt, account ownership increased by 10 percentage points for women and 12 percentage points for men, narrowing the gender gap from 58 percent in 2024 to 40 percent in 2025. However, progress remains uneven elsewhere, with no material change recorded in Ethiopia and stagnation observed in India since 2023.

Rural divide and structural barriers limit adoption

The gender gap is further amplified by geography. In five out of ten surveyed countries, disparities are wider in rural areas. Nigeria reflects this divide, with a 35 percent gap in rural areas compared to 16 per cent in urban centres.

Other countries show similar patterns, including Ethiopia (62 percent rural versus 47 percent urban), Pakistan (74 percent versus 42 percent), India (64 percent versus 53 percent), and Sri Lanka (64 percent versus 13 percent). Egypt stands out as an exception, where the gender gap is narrower in rural areas than in cities.

Beyond geography, behavioural and structural barriers continue to limit adoption. Across markets, the most cited obstacles include a perceived lack of relevance of a mobile money account (specifically a preference for cash) and a lack of knowledge and skills.

Women are disproportionately affected. In several countries, more women than men report lacking knowledge of how to use mobile money. For instance, in Ethiopia, 60 percent of women cite lack of knowledge as a barrier compared to 54 percent of men. Similar trends appear in Bangladesh, India, and Egypt.

Additional challenges include handset usability and literacy gaps. The report notes that overall literacy is a greater challenge for women than men in countries such as Ethiopia and Bangladesh, further constraining access.

Preferences for cash also skew more heavily among women. In Pakistan, 76 percent of women cite cash preference as a barrier compared to 64 percent of men, while similar gaps are observed in Egypt and Bangladesh.

Usage gaps persist beyond account ownership

While Nigeria’s progress in closing the ownership gap is notable, disparities remain in how mobile money is used. Globally, women are less likely than men to actively use their accounts, particularly over shorter timeframes.

The report observes that “in nearly all countries, the 7-day activity gender gap exceeds the 30-day activity gap,” indicating that gender disparities become more pronounced with frequent usage.

Nigeria, however, shows signs of improvement. “The country recorded a reduction in the 30-day activity gender gap by 11 percentage points, alongside a 12 percentage point increase in women’s activity rates. The 7-day activity gap also narrowed by 19 percentage points, suggesting stronger engagement among female users,” it said.

Read also: M-PESA Ethiopia pioneers Africa’s first mobile money AI bundle

Despite this progress, differences persist in the range of services used. Women are consistently less likely than men to engage in multiple types of transactions.

The report noted that women are less likely than men to have performed three or more different types of transactions over the past seven days, highlighting a gap in the depth of financial participation.

“This disparity extends across everyday financial activities, including sending money, paying bills, making merchant payments, and receiving income. Even in more advanced markets, gaps remain in frequent and diverse usage, showing that access alone does not guarantee equal participation,” the GSMA report stated.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp