Guaranty Trust Holding Company (GTCO) Plc continues to demonstrate why it remains a bellwether for the Nigerian banking sector. GTCO pairs robust fundamental growth with an aggressive dividend strategy that keeps investors leaning bullish.

Following its recent full year (FY) 2025 audited results, where the Group posted a Profit Before Tax (PBT) of N1.23 trillion, the case for further upside in its share price rests on three core pillars.

First is that with a best-in-class cost-to-income (CIR) ratio of 27.9percent, GTCO continues to extract more value from every Naira earned than its Tier-1 peers, ensuring that topline growth translates effectively into shareholder wealth.

Again, despite a volatile macroeconomic backdrop, the Group has successfully de-risked its balance sheet, maintaining a low Cost of Risk (2.2percent) and a healthy Stage 3 loan ratio, which provide a sturdy floor for valuation.

Also, the declaration of a N12.76 per share annual dividend (representing a double-digit yield at current prices) not only rewards long-term holders but also creates a persistent “buy” signal for income-seeking institutional investors.

There has been intense activity in the stock recently signaling strong institutional positioning.

Beyond the cash flow, GTCO’s stock has seen a sharp re-rating in early 2026. Several factors are driving the share price toward analyst targets. First is that GTCO successfully met the Central Bank of Nigeria’s (CBN) new capital requirements well before the March 31, 2026 deadline. This removed the regulatory risk overhang that had suppressed the stock’s valuation before March 31 deadline.

Another is the bank’s digital ecosystem growth. The “Habari” super-app and the group’s non-banking subsidiaries (HabariPay, Pension, and Funds Management) now contribute majorly to Group Profit Before Tax (PBT). Investors are now valuing GTCO as a diversified fintech/holding company rather than just a traditional lender.

Also, with a Cost-to-Income Ratio (CIR) of 27.9percent, GTCO remains one of the most efficient financial institutions in the world. This allows more profit to flow directly to shareholders.

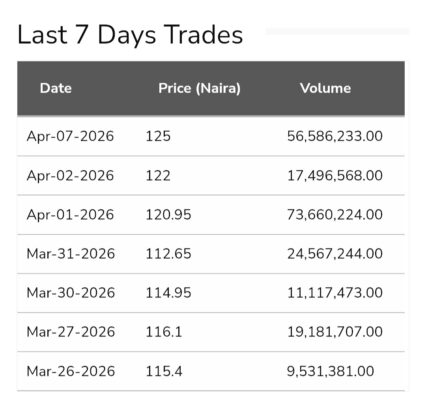

GTCO currently trades near its 52-week high of N127.5 as against a 52-week low of N56.95. GTCO often trades at a Price-to-Earnings (P/E) ratio of approximately 4.7x, which many analysts consider undervalued given its high growth and profitability metrics. After trading on Tuesday, April 7, the stock reached a high of N125 rising by N3 or 2.46 percent as against N122 it traded the preceding day.

Due to GTCO’s transparency and corporate governance, the stock remains a staple in the portfolios of foreign institutional investors and local pension fund administrators. Domestic retail investors are also note left out in the scramble for the share.

In its Audited Consolidated and Separate Financial Statements for the year ended December 31, 2025, Guaranty Trust Holding Company Plc reported profit before tax (PBT) of N1.23trillion underpinned by strong growth in core earnings, with interest income and fee income increasing year-on-year (y-o-y) by 23.2 percent and 25.9 percent, respectively.

The results released to the Nigerian Exchange Limited (NGX) and London Stock Exchange (LSE) show the Group performance reaffirms its capacity to generate sustainable earnings and builds on the momentum from 2024, when GTCO delivered a record profit of N1.27trillion, driven in part by N517.5billion in fair value gains, which did not recur in 2025.

The Group’s 2025 profit after tax came in at N865.75billion against N1.02trillion recorded in 2024. The profit after tax reflects the impact of recent fiscal policy adjustments to the taxation of investment securities, notably withholding tax on short-term instruments. However, when normalised for this effect, underlying earnings remain robust, driven by growth in core operating income.

The Group continues to maintain a well-structured, healthy, and diversified balance sheet in all the jurisdictions wherein it operates a Banking franchise, as well as across its Payments, Pension and Funds Management business verticals.

Total assets and shareholders’ funds closed at N17.8trillion and N3.4trillion, respectively. Capital Adequacy Ratio (CAR) remained very robust and strong, closing at 43.8 percent, likewise asset quality improved as evidenced by IFRS 9 Stage 3 Loans which closed at 3.4 percent and 5 percent at Bank and Group level in FY-2025 (Bank, 3.5 percent, and Group, 5.2 percent in December 2024).

Cost of Risk (COR) also improved to 2.2 percent from 4.9 percent in December 2024. In specific terms, the Group’s loan book (net) grew by 12.4 percent from N2.79trillion as of December 2024 to N3.13trillion in December 2025.

Similarly, deposit liabilities grew by 23.8 percent from N10.40trillion to N12.87trillion during the same period.

Overall, the Group continues to post one of the best metrics in the Nigerian Financial Services Industry in terms of key financial ratios that is: Post-Tax Return on Equity (ROAE) of 28.3 percent, Post-Tax Return on Assets (ROAA) of 5.3 percent, Capital Adequacy Ratio (CAR) of 43.8 percent and Cost to Income Ratio of 27.9 percent.

“Our 2025 result underscores the resilience and depth of our earnings capacity. Following a record 2024, which included significant fair value gains, our focus has been on strengthening the sustainability of our earnings by driving growth across our core banking and ecosystem businesses,” said Segun Agbaje, Group Chief Executive Officer of Guaranty Trust Holding Company Plc.

He said “The strength of our underlying earnings, despite a stronger Naira and tighter regulatory parameters, reflects the quality of our franchise and the discipline with which we execute our strategy. Importantly, this strong core earnings performance underpins our capacity to sustain and grow shareholder returns.

“Our record dividend payout this year is not only a reflection of our current profitability but also of our confidence in the Group’s long-term earnings potential. Looking ahead, we remain focused on scaling our ecosystem, driving innovation across our financial services platform, and delivering consistent, high-quality earnings that support superior value creation for our shareholders,” Agbaje noted.

In their recent note, Lagos-based Coronation research analysts said, “Guaranty Trust Holding Company (GTCO) delivered a mixed but broadly resilient performance in FY 2025, underpinned by strong balance sheet expansion, robust growth in non-interest income, and improved asset quality, albeit pressured by margin compression, weaker trading income, and a normalisation in earnings after the exceptional gains recorded in the prior year”.

“The group proposed a final dividend of N11.76 per share for FY 2025, bringing the total dividend for the year to N12.76 per share (FY 2024: N8.03). Based on the current market price, this translates to an attractive dividend yield of approximately 9.7 percent,” they noted.

Also, CardinalStone research analysts said their target price for GTCO is shares is N136.91. “GTCO’s core performance was stronger in FY’25, with Net-Interest Income rising 19.1percent YoY to N1.3 trillion, benefiting largely from a 28 percent YoY expansion in Interest Earning Assets (IEA) to N12.7 trillion,” they added.

GTCO consistently delivers high returns on the capital shareholders have invested. Analysts project a Return on Equity of 32.1 percent over the next three years, which is substantially higher than the Nigerian banking industry average of roughly 21.5percent. The Group’s healthy balance sheet with a Capital Adequacy Ratio (CAR) of 43.8percent as at FY’2025 provides a massive buffer against economic shocks.

While the broader NGX All-Share Index (ASI) is up approximately 30 percent year-to-date (YtD), GTCO remains a primary driver of the banking sector’s performance, consistently testing new all-time highs as it nears the N130 resistance level.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp