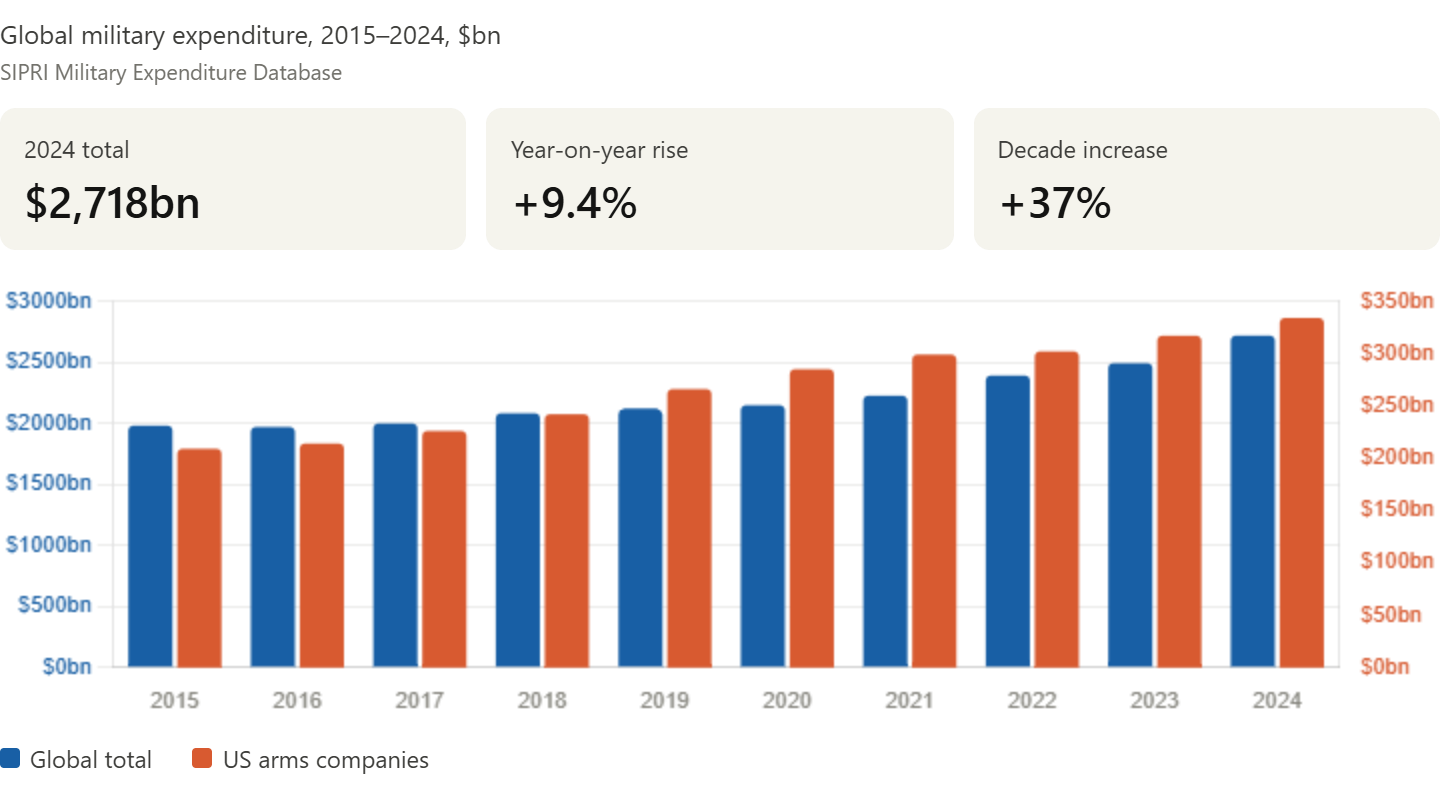

War is first a human tragedy, but markets do not read history through grief. They read it through orders, contracts, fuel prices, insurance premiums, shipping delays and government budgets. That is the uncomfortable starting point for any serious discussion of the economics of war. SIPRI estimates that global military expenditure rose to $2.718 trillion in 2024, the highest level on record, with spending up 9.4 per cent in one year and 37 per cent over the past decade. In plain terms, the world is not merely living through isolated conflicts; it is operating in an era of sustained rearmament. That matters because once military spending rises and stays elevated, whole industrial ecosystems begin to adjust around it. Factories expand, procurement pipelines lengthen, stock markets re-rate defense names, and the incentives of finance move quietly alongside the incentives of strategy. The moral horror of war and the commercial logic surrounding it often coexist in the same moment, and that is precisely why the subject deserves clear-eyed economic analysis rather than sentiment alone.

Why defense firms attract capital in wartime

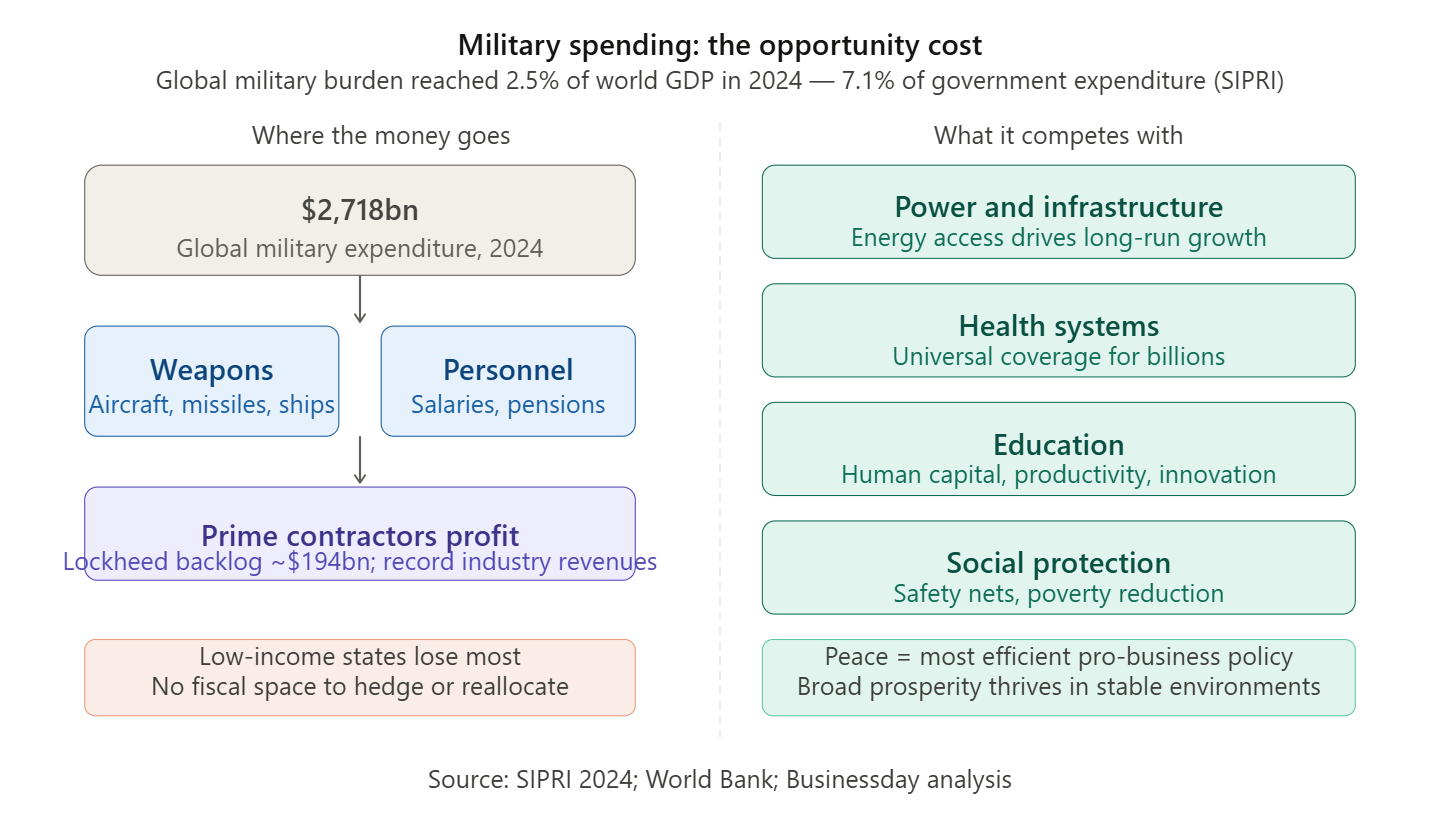

This is why companies such as Lockheed Martin sit at the centre of the conversation. Lockheed is not just another industrial name; it is a prime contractor on the F-35 programme and a major supplier of missile and air-defense systems at a time when governments are replenishing stockpiles and revising security doctrine. SIPRI says revenues from the world’s 100 largest arms-producing companies reached a record $679 billion in 2024, while U.S. arms companies alone generated $334 billion. Lockheed itself reported a record backlog of about $194 billion after 2025, alongside rising sales and management commentary pointing to “unprecedented demand” for its capabilities. Reuters reported in January 2026 that the company projected stronger 2026 revenue and profit, supported by robust demand for missiles, air defense systems and fighter aircraft. In other words, investors are not reacting to one headline or one missile strike in isolation. They are pricing the expectation that geopolitical instability will produce multi-year public spending commitments, stronger order books and longer earnings visibility for defense contractors.

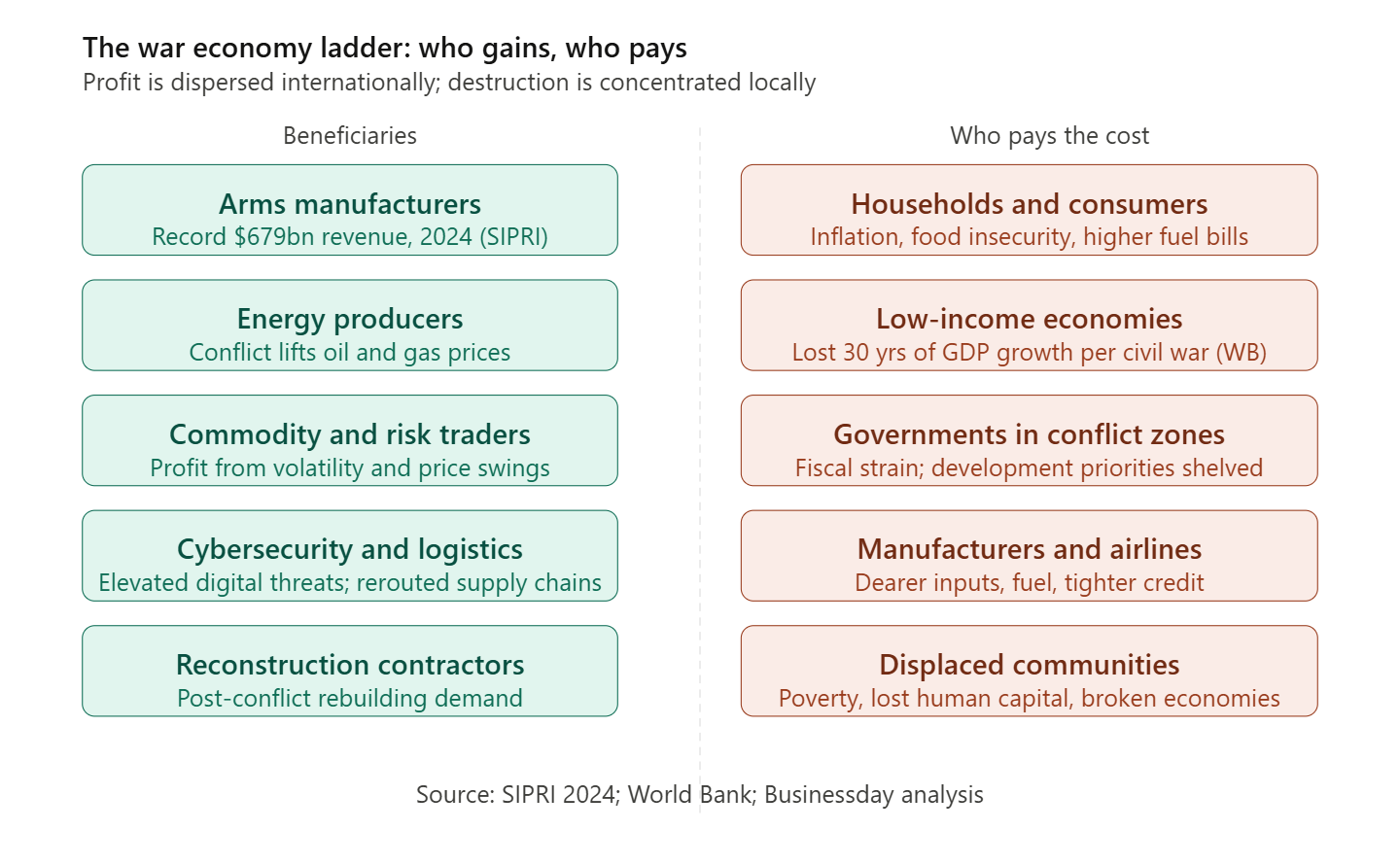

The winners are not only arms makers

Still, to say that war benefits defense manufacturers is true but incomplete. The beneficiaries of war extend far beyond weapons firms. Energy producers may benefit when conflict lifts oil and gas prices. Commodity traders profit from volatility. Shipping insurers earn more as risk premia rise. Cybersecurity companies gain from elevated digital threats. Logistics firms, satellite operators and reconstruction contractors can all find new demand in the wake of military escalation. Even diversified global asset managers may end up exposed to many sides of the same conflict economy because their portfolios hold defense, energy, industrial, transport and technology stocks simultaneously. This is why war should be understood as a system-wide economic shock, not merely a battlefield event. It destroys homes, lives and public finances in affected regions, yet it can create revenue surges, valuation uplifts and strategic opportunities in boardrooms far removed from the front line. The economic map of war is therefore uneven: devastation is concentrated locally, while profits are often dispersed internationally through capital markets and supply chains.

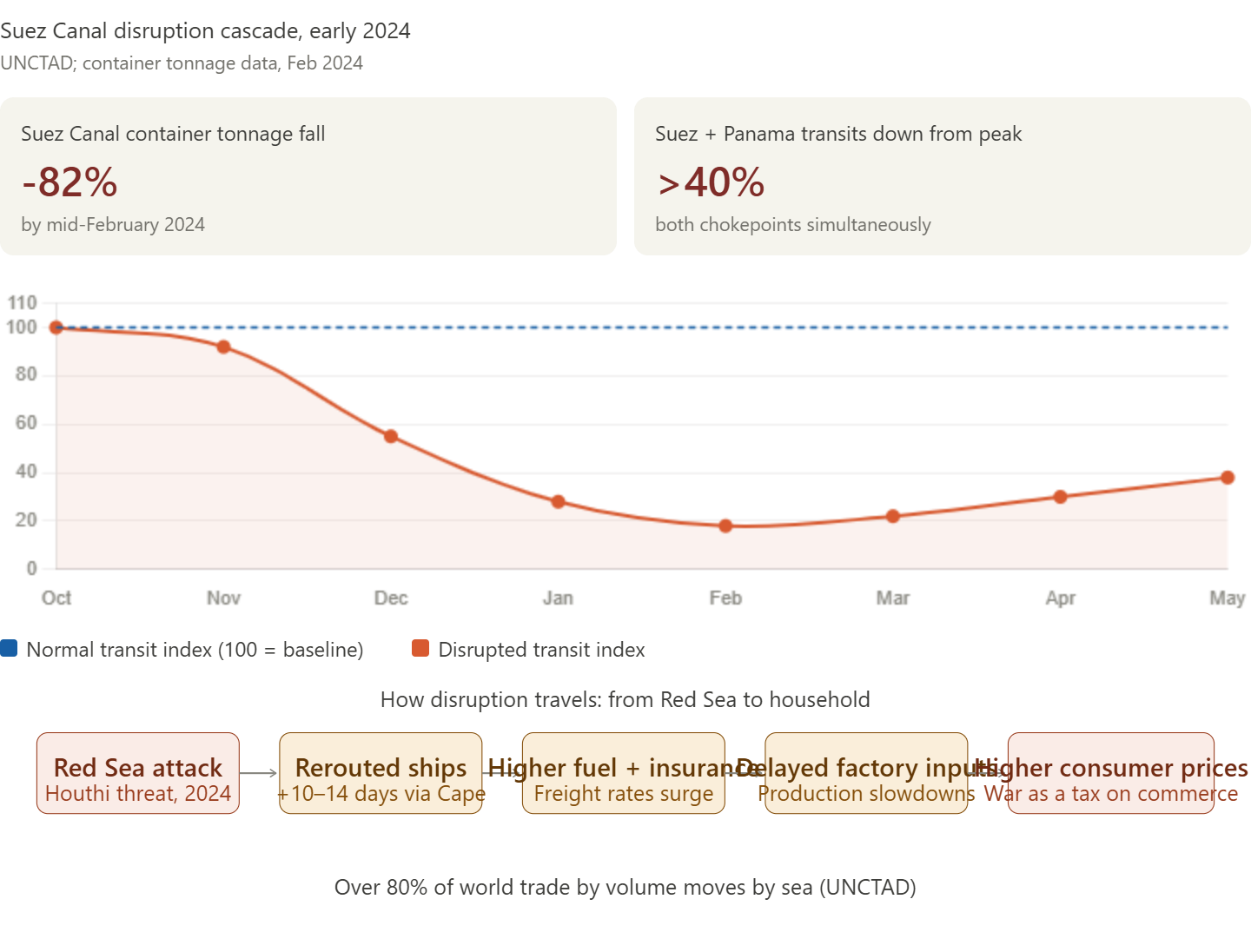

How conflict spreads through prices, trade and inflation

The wider economy pays a price for this arrangement. Conflict does not stop at the battlefield; it leaks into freight routes, fuel bills, food prices and monetary policy. UNCTAD warns that key maritime chokepoints such as the Suez Canal are increasingly vulnerable to geopolitical tensions and that these disruptions extend shipping routes, strain supply chains and raise costs across the global economy. It notes that over 80 per cent of world trade by volume is carried by sea. In early 2024, as Red Sea disruptions intensified, transits through the Suez and Panama canals were both down by more than 40 per cent from prior peaks, while container tonnage crossing the Suez had fallen 82 per cent by mid-February. These are not abstract numbers. Longer routes mean higher fuel use, more expensive insurance, delayed inputs for factories and rising prices for consumers. In that sense, war acts like a tax on commerce. Someone earns from the disruption, but most businesses and households simply absorb the cost through thinner margins and more expensive living.

The burden falls hardest on poorer economies

The heaviest burden usually lands on countries least able to bear it. The IMF warned this week that war in the Middle East points in one broad direction for the world economy: higher prices and slower growth, with low-income countries especially vulnerable to food insecurity and tighter financial conditions. The OECD’s latest interim outlook reaches much the same conclusion, projecting global growth of 2.9 per cent in 2026 and saying the energy shock tied to the conflict would raise G20 inflation by 1.2 percentage points relative to earlier projections. The World Bank has long warned that a civil conflict can cost the average developing country roughly 30 years of GDP growth. That single insight captures the asymmetry of war economics. Richer economies may be able to hedge, insure, subsidise or reallocate. Poorer economies import the inflation, suffer the fiscal strain and watch development priorities slide backward. For many of them, war elsewhere still means hunger at home, more expensive fertilizer, weaker currencies, rising debt distress and one more delay in the long journey out of poverty.

What governments must learn from the new war economy

Governments therefore need a more disciplined approach to national security spending. Defense outlays will remain necessary in a dangerous world, but procurement without transparency quickly becomes a transfer mechanism from taxpayers to politically connected suppliers. States should build military readiness through competitive contracting, stronger parliamentary oversight, realistic stockpile planning and more resilient local maintenance capacity. They should also measure the opportunity cost of security spending with greater honesty. Every extra budgetary allocation to defense competes with power, transport, health, education and social protection unless revenues rise accordingly. That trade-off is becoming sharper as military expenditure consumes a bigger share of public resources. SIPRI says global military burden rose to 2.5 per cent of world GDP in 2024 and average military spending reached 7.1 per cent of government expenditure. Those are not trivial ratios. Smart governments must resist the temptation to let fear write blank cheques. Security policy should protect national stability, not become an open-ended business model that enriches contractors while weakening the social foundations of long-term growth.

What investors and organised private sector should understand

Investors also need to think beyond the easy narrative that war automatically makes defense stocks a one-way trade. Yes, geopolitical tension can support order books and valuations, but war also brings cost overruns, delivery bottlenecks, political scrutiny and policy unpredictability. SIPRI notes that even as arms revenues surged, major U.S.-led programmes such as the F-35 continued to face delays and budget overruns. In other words, demand strength does not eliminate execution risk. For the organised private sector, the bigger point is that broad-based prosperity thrives in predictable, peaceful environments, not in permanent crisis. A few listed firms may gain from militarisation, but most businesses suffer when shipping is disrupted, energy prices spike, inflation persists and borrowing costs rise. Manufacturers face more expensive inputs, airlines face higher fuel bills, banks face tighter financial conditions, and consumers pull back as real incomes weaken. Business associations should therefore advocate not only for security, but for diplomacy, supply-chain resilience and regional peace architecture. Peace is not merely a moral aspiration; it remains the most efficient pro-business policy available to any serious economy.

The final truth about who benefits

So who are the beneficiaries of war? The honest answer is that war creates a ladder of beneficiaries and victims. At the top are arms producers, selected energy interests, risk traders, logistics intermediaries and financial investors positioned on the right side of volatility. At the bottom are households, displaced communities, fragile states and budget-constrained governments that pay in inflation, poverty and lost development. Between those poles lies the central economic lesson. War can generate profit, but it rarely creates broad prosperity. It can lift individual balance sheets while damaging collective welfare. It can produce stock market winners even as it deepens public loss. That is why economists must describe war with sobriety. The issue is not whether markets respond positively to rising defense demand; they do. The real issue is whether societies are prepared to see through the market’s cold arithmetic and remember that what appears as revenue on one balance sheet often began as destruction somewhere else. That is the true economics of war, and it is why peace remains humanity’s best long-term investment.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp