Wars once took years to reshape the global economy. In 2026, it took just 50 days.

What began as a military escalation involving the United States, Israel and Iran quickly evolved into a market shock that rippled across oil, shipping, inflation expectations and investor positioning. Brent crude surged from about $72 a barrel before the conflict to a peak above $118, a rise of more than 60 percent, according to market data compiled in a conflict timeline by ARM Research.

For policymakers, investors and consumers, the message was immediate. In a global system defined by tight supply chains and fragile geopolitics, even short conflicts can trigger broad macroeconomic repricing.

Oil moved first and set the tone

Energy markets were the first to react, and the most aggressively repriced.

As strikes intensified and tensions mounted around the Strait of Hormuz, traders began pricing in supply disruption risk. The strait remains one of the world’s most critical energy corridors, carrying a large share of global crude and LNG flows.

That vulnerability was enough.

Even partial disruption risk triggered a sharp rally in Brent crude, pushing it above $118 a barrel, one of the steepest short-term increases since the post-pandemic energy shock. LNG prices in Asia also climbed as freight costs, insurance premiums, and rerouting risks increased.

Sheriff Abdulsalam, a corporate finance and alternative investment specialist, said the market response reflected a structural shift in energy pricing.

“Energy markets are no longer pricing only supply and demand. They are pricing disruption probability, route security, and escalation risk. That is why even short-lived conflicts can trigger large and fast repricing.”

Inflation expectations turned quickly

The second transmission channel was inflation.

Before the escalation, many central banks were preparing for a gradual easing cycle as inflation cooled. The oil shock disrupted that trajectory.

Energy is a fast-moving input into transport, food distribution, manufacturing, and household consumption. As crude prices surged, inflation expectations adjusted almost immediately.

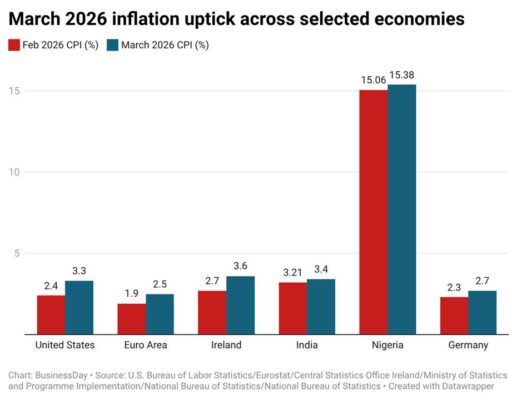

The March data reflected that shift across multiple economies. In the United States, inflation rose to 3.3 percent from 2.4 percent in February. In the Euro Area, it increased to 2.5 percent from 1.9 percent. Ireland moved to 3.6 percent from 2.7 percent. India edged up to 3.4 percent from 3.2 percent. Nigeria, where disinflation had lasted 11 consecutive months, saw headline inflation rise to 15.38 percent from 15.06 percent, according to the National Bureau of Statistics.

Abayomi Fashina, a risk analyst at STL, said the shift was less about the data point and more about expectation reordering.

“The conflict reintroduced a risk premium into inflation forecasts. Markets that had priced in rate cuts began reassessing whether central banks would delay easing cycles.”

Bond yields rose across several markets during the peak of the crisis, while expectations for aggressive rate cuts softened.

Safe-haven flows returned at speed

As geopolitical risk escalated, capital repositioned quickly.

Gold strengthened as investors sought protection. The US dollar gained on haven demand. Equity markets weakened during the early phase of the conflict, while defence-related stocks outperformed on expectations of higher military spending and sustained geopolitical tension.

The pattern itself was not new. What changed was the speed.

Portfolio adjustments that once unfolded over weeks now occurred within days, driven by algorithmic trading systems and real-time geopolitical feeds.

Shipping became the transmission channel most markets underpriced

While oil dominated headlines, shipping markets carried one of the most important secondary shocks.

Freight and insurance costs for vessels crossing the Gulf rose sharply as risk premiums were recalibrated. Even limited threats to the Strait of Hormuz typically force rerouting decisions, longer voyage times, and higher insurance coverage costs.

That matters because modern inflation is not transmitted only through commodity prices, but through logistics friction.

A delayed cargo can propagate cost increases across energy, food imports, and industrial supply chains. In that sense, shipping disruption acts as a multiplier of the oil shock extending its reach beyond energy markets into broader price structures.

Why 50 days changed the macro cycle

The core lesson of the episode lies in compression.

Economic effects that previously unfolded over months or years now materialise within weeks. Energy prices, inflation expectations, currency flows, and asset allocation decisions now respond almost simultaneously to geopolitical signals.

Technology has accelerated this process. Markets now process satellite imagery, shipping data, military developments, and news flows in real time. Capital responds within minutes rather than policy cycles.

This creates a structural challenge for central banks and governments: macroeconomic policy is still slow-moving, but the shocks it responds to are increasingly instantaneous.

The world after the ceasefire

When a ceasefire eventually emerged, oil prices eased back toward the mid-$90 range and risk assets partially recovered, according to the ARM market timeline. But the full reversal did not occur.

Markets rarely forget how repricing happens.

What remained was a higher geopolitical risk premium embedded across energy, shipping, inflation expectations, and asset allocation models. Investors had observed how quickly a narrow chokepoint or short escalation could ripple through global pricing systems.

The implication is structural.

Geopolitical risk is no longer a background variable. It is a live pricing input.

The age of slow-moving economic shocks is fading. In its place is a system where a matter of weeks, sometimes days is enough to reset global inflation paths, investment assumptions, and policy expectations.

Wars no longer need years to reshape the world economy. In a tightly connected system, 50 days can be enough to do the job.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp