Nigeria is moving to tax company profits that are kept within the business rather than paid out to shareholders, ending a long-standing practice that allowed firms to defer tax by retaining earnings.

The change means companies may now face tax on retained earnings even when no dividend is declared, as authorities are empowered to treat certain undistributed profits as if they had already been paid to shareholders.

The new law gives tax authorities the power to go beyond declared dividends. According to Section 10 of the NTA, “Where a Nigerian company has not distributed profits, the Service may direct that the proportion which could have been distributed be construed as distributed.”

Read also: Ecobank Nigeria reports $31m pre-tax loss as Group profit rise by 22%

The Act further provides that such profits “shall constitute a taxable income in the hands of individual shareholders,” effectively bringing undistributed earnings into the tax net.

This means companies can now be taxed on profits even if they have not been paid out, removing the long-standing ability to defer tax by retaining earnings.

Tax experts say the new provisions align Nigeria with global efforts to curb base erosion and profit shifting, where companies move profits to low-tax jurisdictions or delay distributions to reduce tax exposure, and could result in higher effective tax payments.

“This change reduces the flexibility companies had in holding back profits without immediate tax implications,” said Yvonne Afolabi, a transfer pricing expert. “It may require more deliberate tax planning around dividend policies and reinvestment strategies.”

This means that companies can no longer freely hold back profits to delay tax; they now have to carefully plan when to distribute or reinvest earnings because tax authorities can step in and tax those profits anyway.

Read also: Nigeria turns wealthy lifestyle habits into tax funnel

The provision represents a major shift from Nigeria’s previous tax framework, where retained earnings were largely outside the tax net unless distributed.

While reforms in 2019 reduced cases of double taxation, the system still allowed companies to defer tax by holding profits in reserves.

Under the new law, that window is narrowing. The Act introduces “deemed distribution” rules, allowing tax authorities to reclassify profits as distributed where companies, particularly those controlled by a small group of shareholders, retain earnings that could have been paid out without harming operations.

In such cases, the profits are taxed in the hands of shareholders in proportion to their ownership.

It also extends Nigeria’s tax reach beyond its borders. Through newly introduced Controlled Foreign Corporation (CFC) rules, profits retained by foreign subsidiaries of Nigerian companies can now be deemed distributed and taxed locally, especially where those profits are held in low-tax jurisdictions or not subject to a minimum effective tax rate.

“This eliminates the deferral advantage often used in tax planning and ensures profits that economically belong to Nigerian entities are taxed in Nigeria,” analysts at KPMG said in a recent review of the law.

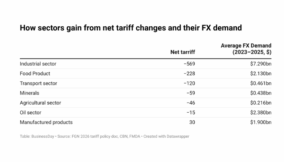

The shift comes as authorities intensify efforts to boost revenue in an economy where tax collection remains relatively low compared to output. Data from the National Bureau of Statistics show that company income tax (CIT) rose sharply to N9.21 trillion in 2025, up from N3.13 trillion in 2024, reflecting both improved compliance and stronger enforcement.

Ten key sectors, including finance, manufacturing, and telecommunications, accounted for N4.57 trillion of collections, emphasising the contribution of corporate taxes to government revenue.

The shift increases pressure on companies to justify retained earnings, especially when they could have distributed profits without affecting operations.

Read also: Here are top 10 sectors that paid the most tax in 2025

However, the changes are not without concern. Analysts say the broader discretion granted to tax authorities could create uncertainty for businesses, especially those that retain earnings for legitimate purposes such as expansion, capital expenditure, or debt servicing.

The provision also fits into a wider overhaul of Nigeria’s tax framework. The law reinforces a move toward a worldwide income system, under which profits earned by Nigerian companies are taxable regardless of where they are generated, received, or held. Nigerian parent companies may need to pay the difference locally if foreign subsidiaries fall below a prescribed minimum effective rate.

For multinational firms and closely held companies, the implication is clear: profit retention strategies will face closer scrutiny, and structures designed to defer tax could trigger additional liabilities.

Analysts say the effectiveness of the new rules will depend on transparent and consistent enforcement. While the provisions could strengthen revenue and improve tax fairness, unclear interpretation risks raising compliance costs and discouraging investment if businesses perceive the system as unpredictable.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp