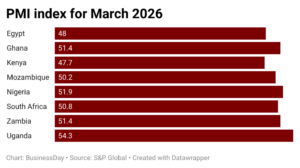

…fell to 47.7 in March 2026, weakest in Africa

Kenya’s private sector activity slipped to its weakest level in eight months in March 2026, as fallout from the Middle East conflict squeezed demand, disrupted logistics and intensified cost pressures across the economy.

The latest Purchasing Managers’ Index (PMI) released on Tuesday from S&P Global showed the headline index fell to 47.7 from 50.4 in February, marking its first contraction since August and signalling a deterioration in business conditions. A reading below 50.0 indicates a contraction in activity.

The decline also extends a broader softening trend, with the PMI now falling for four consecutive months. As a high-frequency gauge of economic momentum, the index often mirrors broader shifts in Gross Domestic Product (GDP), showing the growing fragility in East Africa’s largest economy.

Weakest performer in Africa

Further analysis of eight major African economies surveyed last month shows Kenya recorded the weakest business conditions on the continent. This marks a reversal from February, when Ghana posted the softest reading despite historically low inflation.

“Kenya’s private sector showed clear signs of cooling in March, as businesses reported a solid decline in both output and new orders following six months of expansion,” the index report said.

Firms attributed the slowdown to tighter household budgets, reduced cash circulation and more cautious consumer spending. External shocks linked to the Middle East conflict also exacerbated the downturn, with businesses citing logistics bottlenecks and rising fuel and transport costs.

Demand weakens, costs rise

Survey data show the first decline in total new orders in seven months, prompting firms to scale back output. The contraction in demand reflects mounting pressure on household incomes, as inflationary spillovers from higher energy prices begin to bite.

While input costs accelerated in March, businesses largely refrained from passing these increases on to consumers, highlighting the fragility of demand.

According to Stanbic Bank Kenya, which compiles the survey, although some firms continued to record growth—supported by marketing, innovation and digital sales channels—a larger share reported financially constrained customers and declining order volumes.

Businesses also flagged disruptions to international shipping routes linked to the conflict, further weighing on sales and supply chains.

Oil shock reverberates across Africa

The escalation of tensions involving the United States, Israel and Iran since late February has pushed global crude oil prices above $100 per barrel, raising concerns over sustained supply disruptions.

Particular attention has centred on the Strait of Hormuz, a critical chokepoint for roughly a fifth of global oil supply, where tanker traffic disruptions have heightened volatility in energy markets.

For African economies heavily reliant on imported refined fuel, the impact has been immediate. Rising pump prices are feeding through into higher transport, food and production costs, eroding purchasing power and threatening to reverse recent disinflation trends.

A joint report by the African Union and the African Development Bank warns that if the conflict persists beyond six months, Africa’s GDP growth could decline by at least 0.2 percentage points this year. Pre-crisis projections had placed growth at 4.0 percent in 2026 and 4.1 percent in 2027, following 3.9 percent in 2025.

Inflation pressures resurface

Latest data from the Kenya National Bureau of Statistics show inflation rose in March for the first time in three months, driven by higher food and energy costs linked to the external shock.

Food and non-alcoholic beverages rose 7.7 percent, transport costs increased 3.8 percent, while housing and utilities climbed 2.0 percent. Together, these categories account for more than half of the consumer basket, amplifying the impact on household spending.

Labour market resilience masks caution

Despite weaker output and demand, employment conditions remained relatively resilient, supported largely by hiring in the agricultural sector.

“Output and new orders declined in most sectors, implying that businesses expect to be constrained by geopolitical disruptions,” said Christopher Legilisho, economist at Stanbic Bank Kenya.

He noted that backlogs declined and business optimism for the next 12 months weakened, while subdued demand limited growth in purchasing activity and inventories. Delivery times, however, showed some improvement.

“Higher input costs were linked to tax concerns and rising shipping expenses due to the Middle East conflict, but firms were cautious in raising selling prices in a weak demand environment,” he added.

Mixed picture across the continent

Across Africa, PMI readings point to a mixed but generally resilient outlook. Of the eight countries surveyed, six remained in expansion territory, while two—including Kenya—contracted.

Egypt, which recorded the weakest performance in February at 48.9, slipped further to 48.0 as demand softened and price pressures intensified.

Zambia was the standout performer, with its PMI rising to a four-month high of 51.4, supported by stable input costs, lower selling prices and improved business confidence, although firms continued to trim staff amid wage pressures and supply chain constraints.

Uganda retained the strongest expansion for a fourth consecutive month, followed by Nigeria, Zambia, Ghana, South Africa and Mozambique.

Resilient outlook despite headwinds

Looking ahead, survey data point to a degree of resilience in Kenyan business sentiment. The year-ahead outlook for total activity was broadly unchanged from February, with just over a fifth of respondents forecasting growth.

Expectations are anchored on expansion strategies, including opening new branches, ramping up advertising and online marketing, broadening product and service offerings, and increasing investment in capacity and human capital.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp