Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp

BusinessDay

March 16, 2026

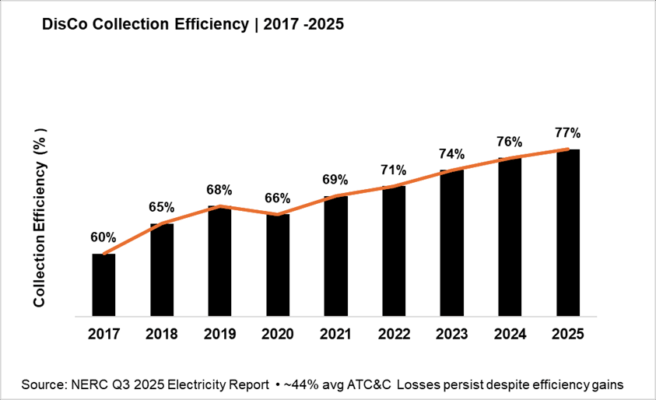

Chart 1: DisCos' Historical Collection Efficiency

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp